An astute reader of last week’s blog post, Equities in Retirement: A 30-Year Case Study, asked a great question: “How much of a maximum decline in annual dividend income (based on prior historical experience) should one be prepared for?” In other words, during dividend bear markets, what level of income decline should we expect?

The obvious answer is that I do not know because even the worst-case historical event is only the benchmark until something even worse comes along. So, it’s wiser for me to say to be prepared for worse than the worst. That being said, I thought it would be valuable to look at the dividend growth pattern over the last 90 years or so to see what insights we can glean from the data.

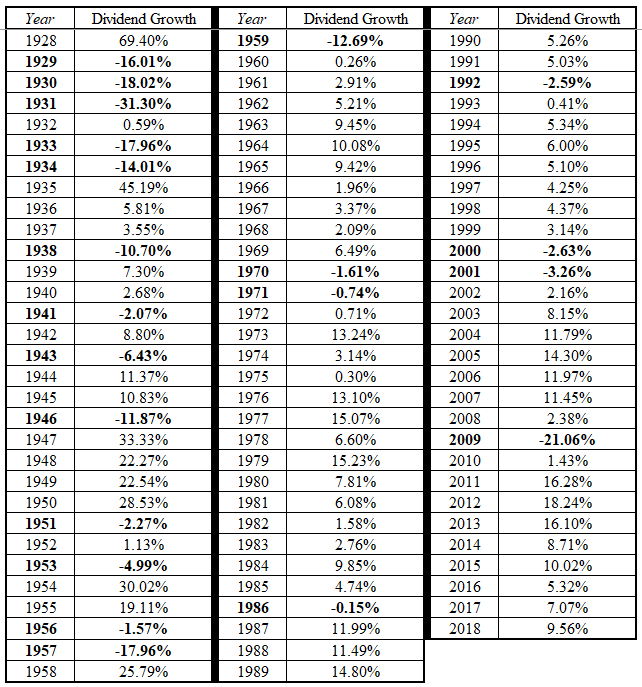

Starting from the top, for obvious reasons, many would expect the dividend picture to look quite bleak in from 1929 into the 1930s. The worst single year for dividend decreases was 1931 with the second-worst being 2009. Not surprisingly, these are much of a result of the 1st and 2nd worst overall market declines in the history of the U.S. market. These were also the only two occasions since 1928 that the dividend decrease exceeded 20%.

There were 21 instances where dividends decreased from 1928 through 2018 or 23% of the years. However, since 1950, dividends have only decreased on 12 occasions or 17% of the time with five of the 12 occurring in the 1950s. This would mean that dividends have decreased only 12% of the time over the last 60 years.

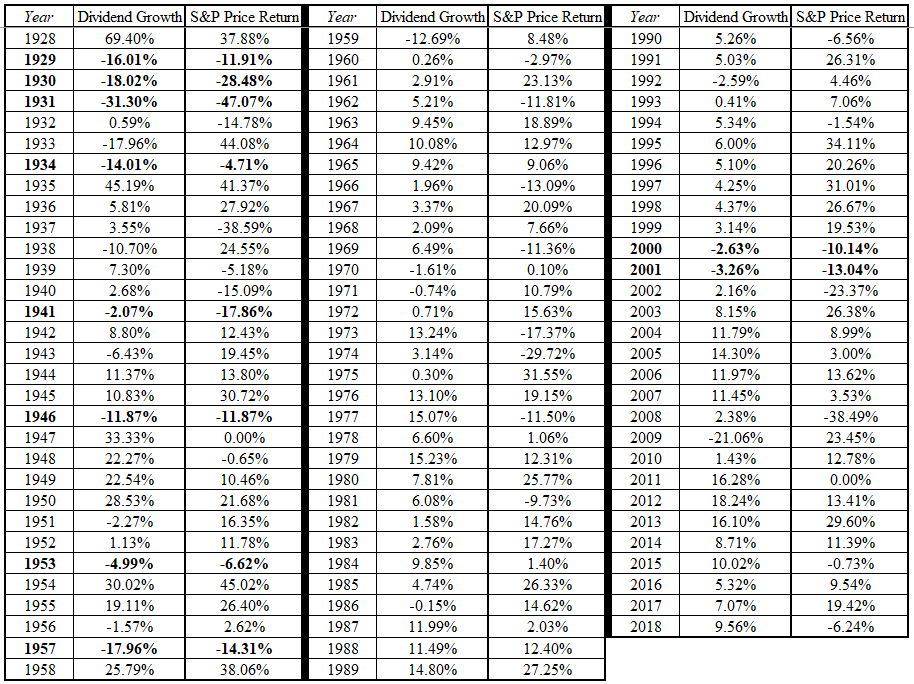

Perhaps even more interesting is that, is over the last 60 years, dividends decreased simultaneously with a market decrease on only two occasions (2000 & 2001) meaning that your decrease would have been somewhat buoyed by a broader market increase in all but those two years. See below.

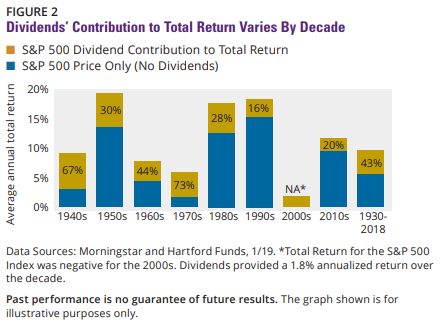

As I reviewed this data, another thing that really stuck out to me was how dividends did through the flat markets of the 1970s and 2000s. It’s intuitive that dividends make up most or all of the return through flat markets as shown below.

But imagine having retired at the beginning of one of those market periods. If you had a dividend income stream to buoy the market volatility, would you have felt better about your income plan?

It is routinely discussed that we are in for an era of lower than average market returns. If that is the case, it would seem that following a dividend growth strategy may be a prudent strategy for that type of environment.

While it’s obvious that I am a proponent of dividend growth for retirement, it’s important to note that dividends are not a panacea. If you are putting together a portfolio strategy for your retirement and a dividend growth strategy is part of your plan, you must acknowledge that dividends are not immune from downturns.

We haven’t had a dividend decrease since 2009 with the average increase from 2010-2018 being over 10%. Thanks to COVID, it may be time for dividends to take an unexpected breather. Only time will tell.

In the end, this is why pairing the dividend growth strategy with a safety net of government/high-quality bonds can be critical to help bridge the gap through dividend bear markets to the inevitable recovery.

Thanks for reading!

Ashby

If you are wondering how to put all the pieces together and think we might be a fit to work together, please feel free to reach out.

This post is not advice. Please see additional disclaimers.