This one is a bit of a softball, and you can probably guess what my answer is. But given that the end of the year was yet another apocalypse du jour and that retirees often worry themselves into making poor portfolio decisions during that sort of event, I wanted to discuss it in more detail.

During the final quarter of 2018, the S&P 500 declined almost 14%. Just prior to 4Q 2018, the financial media was naturally (conveniently?) bullish as the market was peaking in September. But as it reversed course, the media turned decidedly bearish as the market went into another run-of-the-mill intra-year correction. All of a sudden, as if they didn’t even see it coming, this was the newest beginning of the end.

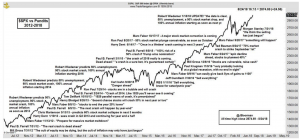

Given the end of the year hysteria, I felt compelled to bring the chart below back into view. This chart, created by Jon Boorman - a technical analyst and portfolio manager for Broadsword Capital, shows just a small sampling of the people that have incorrectly made market calls for what was surely broadcast as the apocalypse. Click here for a larger, more legible image.

If you look closely, you can see the names of some of the smartest minds in the world of finance.

- Bill Gross

- Carl Icahn

- Jeff Gundlach

- Marc Faber

- Robert Wiedemer

For what it’s worth, there are plenty of other market callers that could have made this list just as easily. But what amazes me most about this list is not just how wrong they have all been, but for some of them, how many times they have been wrong and still keep trying to “get it right.” You know what they say though, “A broken clock is still right twice a day,” so eventually they will be too and they’ll say I told you so.

But given my personal mission, what concerns me most is wondering how many retirements have been ruined as a result of heeding their “warnings”?!

I recognize that sometimes there is a fine line between being wrong and being early. But this chart goes back to 2012 and if you recall the phrase “double-dip recession”, you’re probably also aware that this chart could have easily gone back to the Great Panic of 2008 with plenty of other incorrect market calls added to the mix. In reality, it could go back to the very start of financial media.

The great issue here is that this list (and many others who have consistently called for the end of the world) are truly some of the greatest investing minds on planet earth. They live, eat and breathe the stock market. I can all but guarantee that each of these people wakes up thinking about the market and goes to sleep thinking about the market. For many of these folks, it’s their entire existence. And yet, they haven’t even been close to being right.

As Trump was elected late in 2016, I heard many arguments as to why the market was going to fall from clients and other pessimistic investors. And I hear it again and again every time the news channels are shouting from the rooftops that the end is near. But the Trump surprise was far and away the most worried I heard a lot of investors get. I’m not saying that those worries were without merit, but my point to each person I spoke to about it is that we simply do not know what the market is going to do. There is just no way to know that. Period.

Surely, each of the prognosticators above had reasons they believed the markets were at risk, and I’ll bet they were really good reasons. It doesn’t change the fact that they were still wrong. Despite knowing that, what makes us, as individual investors on the periphery of the investing world, think that we know what the market is going to do any more than they do?

I imagine we are relying on the false confidence that many of these pundits have in themselves since most arguments I hear are regurgitations from TV. That doesn’t make them or us any more correct than their records show.

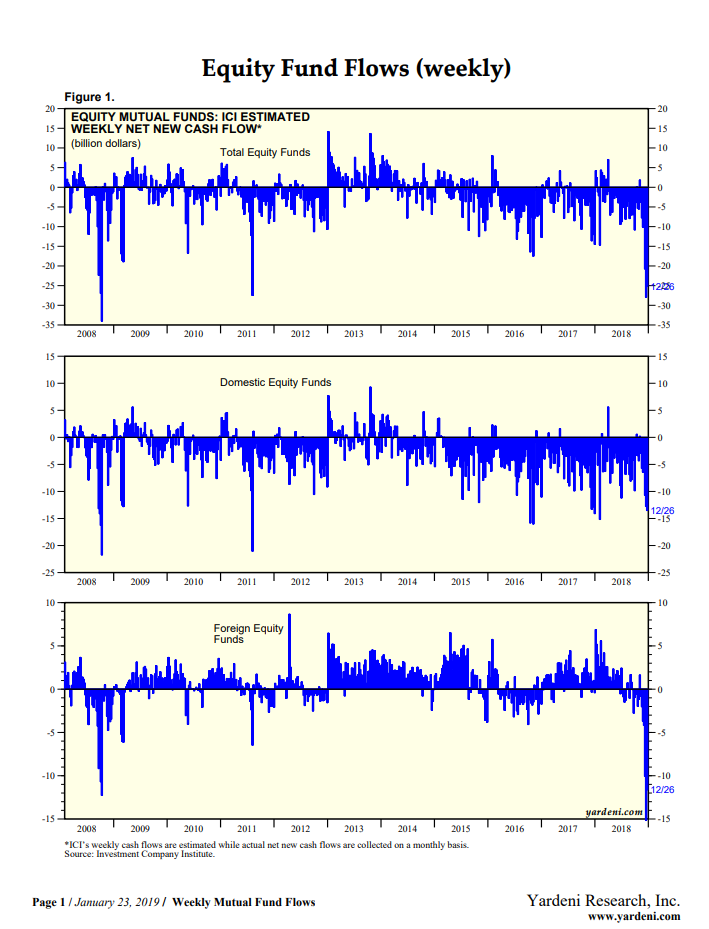

One of my favorite quotes about the market is, “The market has a way of disappointing the greatest number of people.” I do not know who said it, but it seems to ring true on a regular basis. In fact, you can see in the charts below from Yardeni research that people were selling out in droves toward the end of 2018.

Why exactly did people do that? It likely can be summed up in one word - fear. Because apparently, unless you were hiding under a rock (hopefully you were), it probably had something to do with yield curves, fed tightening, and/or tariffs. There was (and is) a veritable buffet of reasons to sell. There always is. Yet, thus far in 2019 as I write this, the S&P is up just over 5.5%.

Legendary investor, Sir John Templeton used to say,

Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.

If fund flows are any indication of investor sentiment, then I’d say we seem to be an awfully long ways from euphoria. Heck, I have to imagine that we are still somewhere between skepticism and optimism. While that quote is 100% subjective, investors that are optimistic or euphoric don’t sell at the first sign of a chink in the armor. To be clear, I am not offering any kind of market forecast either - since I obviously believe those opinions are worth less than zero.

My opinion on financial TV is not to pay much (if any) attention to the pundits. They don’t know what’s going to happen. I don’t know what’s going to happen. And you don’t know what’s going to happen. Because it’s unknowable.

So, what should you do instead?

If this very typical pullback caused you to worry, my best advice might be to stop watching or reading financial commentary, but I realize that’s a big ask for most people. As an alternative, perhaps a useful exercise would be to conduct lifeboat drills on your retirement portfolio.

The point of the lifeboat drill exercise is to ensure that you have enough set aside in non-equity investments to provide the income you’ll need for a certain number of years to allow yourself the patience to wait out the next apocalypse du jour.

For example: If you need $20,000 from your portfolio per year, you might consider placing anywhere from $100,000-$160,000 in a much more stable investment such as short-term, high-quality bonds. The goal is to give you a five to eight-year safety net. Knowing you have that might encourage you to ignore the financial hysteria as it’s happening because you know you can withstand almost anything the market is going to throw at you.

No strategy is perfect because we can’t know what is going to happen in advance. But the best strategy is the one you can actually stick with.

Successfully investing in the Great Companies of America and the World is about establishing a strategy to deal with the inevitable short-term uncertainty that will offer us enough patience to hopefully obtain long-term historical returns. Short-term market uncertainty is not the primary risk. The real risk, as I see it, is making emotional portfolio decisions. Establish a plan to deal with what we already know is coming. Your retirement depends on it.

Thanks for reading!

Ashby Daniels

If you’re looking for a retirement planner to help you make a comfortable transition into retirement and want to see if we’re a good fit, reach out to me and my team at Shorebridge Wealth Management.

Disclaimer: Any opinions are those of Ashby Daniels and not necessarily those of Raymond James. Any information provided is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Investing involves risk and investors may incur a profit or loss.