PLEASE NOTE: This is a long post, but I passionately believe that if retirees have any chance of getting things right, they must properly understand all the underlying assumptions they are making in their retirement planning decision process. And because I view the subject(s) of this particular article to be so important, I wanted all the thoughts in one place instead of being spread amongst three or four individual posts - especially since these issues are inseparable in nature. If you find it thought-provoking and helpful, I’d be thankful if you shared it with someone you care about.

I hear a lot of people in our industry use the phrase, “The risk of living too long,” often referred to as longevity risk. For some reason, it bothers me that we consider living a long life a “risk.” Though it appears that many retirees view it in much the same way given that one of the top fears of retirees today is the possibility of outliving their money.

There are really only two possible outcomes when it comes to your retirement portfolio: You will outlive your portfolio OR your portfolio will outlive you. I believe there are three primary drivers that will determine which outcome you are likely to experience - (1) life expectancy, (2) inflation, and (3) how you choose to invest your funds in retirement.

Establishing legitimate assumptions for life expectancy and inflation is critical and pairing those assumptions with an effective income strategy specifically designed to address those issues is the logical next step. Here, I will address these issues in exactly that order. My hope is by the time you finish this article, you can establish a clear plan for how you might approach your own retirement strategy in a way that might increase your probability of success.

1. Life Expectancy

Because I regularly speak to a variety of retirees and pre-retirees, I always like to ask the question of how long they think they might live? I get it, it’s a morose question, but one that results in a potential chain reaction of decisions that can come back to haunt the retiree.

In having asked that question hundreds of times, the typical answer is in the 80s. To this day, I can’t recall a single person that said they’d live into their 90s, but we’ll get to that in a moment.

Technically, their assumption is correct since the average individual life expectancy for a 65-year-old male today is 83 and for a 65-year-old female is 85. But this estimation is missing three critical pieces of the longevity puzzle. (A) These are the averages. (B) These assumptions totally ignore the idea of “joint life expectancy.” (C) And it ignores continued advances in health care.

If you believe that you will only live into your 80s, then you likely also assume you will only need income for approximately 15-20 years. If that’s your assumption, you may be making different portfolio decisions than you would if you thought you might maintain your health into your 90s or longer? If your assumptions are incorrect, it’s possible your entire retirement income plan is incorrect.

One thing I tell almost every client when discussing our conservative assumptions is, “I’d rather you have it and not need it than need it and not have it.” In other words, if I’m wrong and you have too much money, that’s a much better scenario than being wrong and running out of money sooner than you anticipated.

Planning conservatively for a long life will inevitably cause you to make different assumptions and decisions than you might have otherwise made. Let’s look at some actual longevity information.

(A) The Problem With Averages

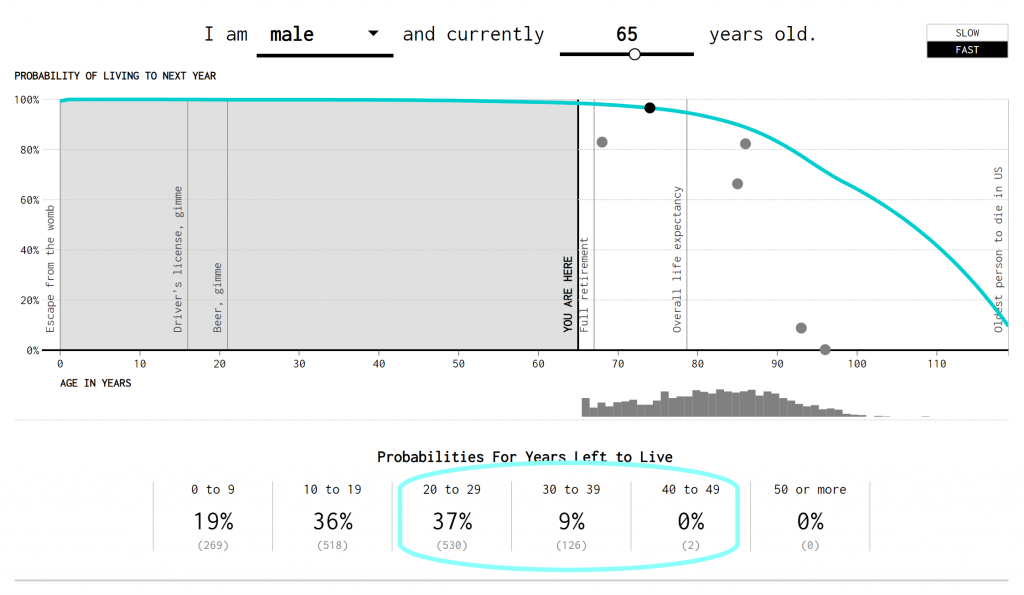

Using life expectancy data from the Social Security administration, Flowing Data created the following interesting visual. I’ve highlighted the “Probabilities for Years Left to Live.” For the average male that is currently 65 years old, approximately 46% will live between 20 and 39 years. A wide range to be sure, but we’re just building an argument here for a moment.

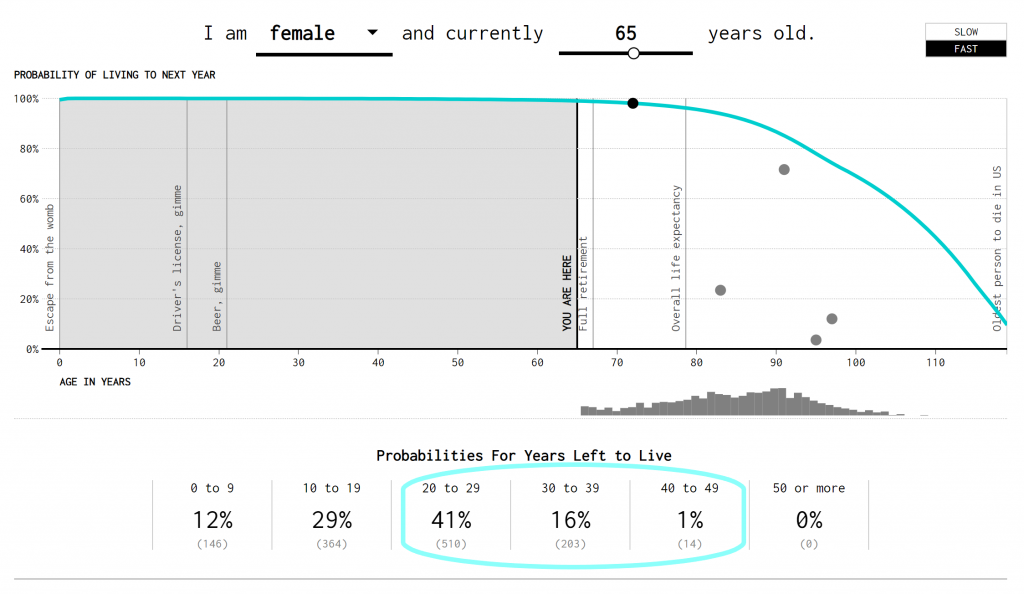

For the average female that is currently 65 years old, approximately 57% will live between 20 and 39 years with an extra 1% living 40 years or more.

Here’s the issue with these two great visuals: they are based on the average male and female. If you are reading this article, there is a high likelihood that you are not average. You’re probably not even close to average.

You’ve likely made an above average income, worked a less physically demanding job, received more and better health care, eaten a healthier overall diet, exercised more, and obtained more education than the average person.

In fact, education may be the most important factor when it comes to individual increased longevity. John Rowe, a professor of public health at Columbia University and former CEO of the insurer Aetna said, “If someone walked into my office an asked me to predict how long he would live, I would ask two things-what is your age and how many years of education did you receive?“

If the circumstances above describe you, it’s at least likely that you will live a longer life than “average” on an individual basis.

But wait there’s more!

(B) Joint Life Expectancy

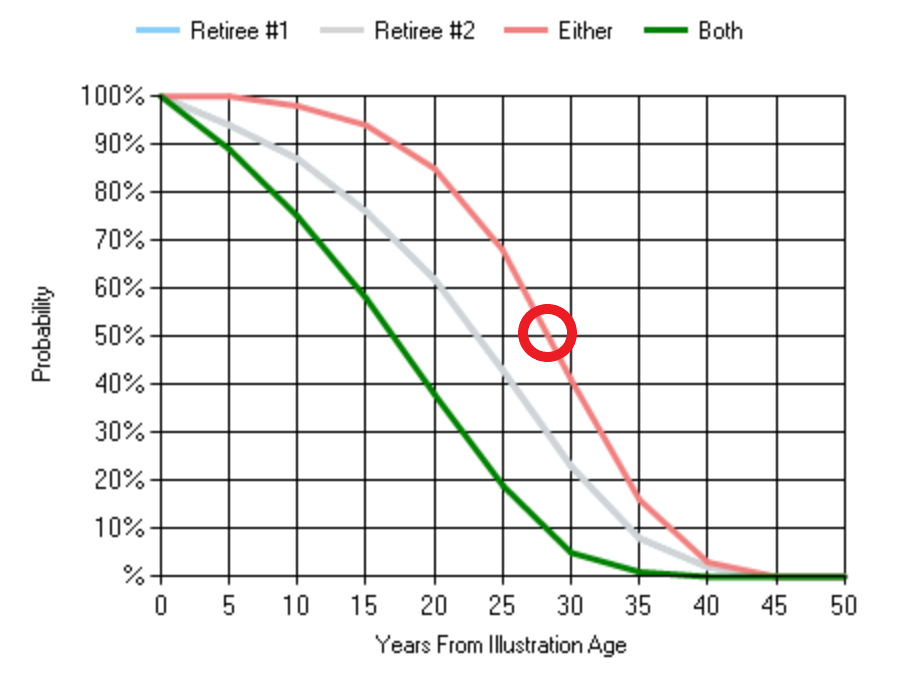

If you were building your retirement plan expectations around the charts above, you may unknowingly be setting yourself up for failure because the estimates above don’t factor in the idea of joint life expectancy. Your joint life expectancy is the age at which the last survivor would then pass away (meaning you or your spouse). As you’ll see in the graph below from the Society of Actuaries longevity calculator, there is apparently something to being married.

The joint life expectancy for a non-smoking couple in good health retiring at age 65 is about 92 or 93 years old.

Let that sink in.

The joint life expectancy is about nine years longer than the individual life expectancy of the average 65-year-old male and almost seven years longer than the average 65-year-old female. I hope you’re beginning to grasp what this could mean when planning for your retirement.

And going back to the “you’re not average” issue above - your joint life expectancy could very well be longer than this!

But wait, there’s more!

(C) Medical Advances

It would be hard to overstate the progress we’re seeing in the field of medicine. It was just announced last month (April 2019) that a group of scientists from Tel Aviv University in Israel have produced a 3D heart using a patient’s tissue via 3D printing technology.

Take a moment and think of the monumental impact that this could have on your own longevity. The technology they used could eventually be capable of replacing your very own heart using your very own cells and tissue - not to mention other body organs that will inevitably follow — this means your body would not reject it because it’s made out of your own cells.

While 3D printing technology began in the 1980s, significant strides in the capabilities of this technology didn’t truly become known until the mid-2000s. Fast forward to today, we’re now “printing” body organs. What do you think is going to happen over the next few decades and how do you think this is likely to impact your longevity?

I’ve not even touched on the increased diagnosing accuracy of Artificial Intelligence or a variety of other medical advances that will almost certainly further extend our lifespans.

Long story short, if long life is, thankfully, more or less inevitable for many of us, what is the obvious issue that needs to be addressed within a good retirement income plan?

2. Inflation

Inflation is more or less ignored by the average retiree despite the price of just about everything tripling during their working years. This is likely because while the prices were tripling, their income was increasing at a faster pace, so it almost didn’t matter. In other words, you could afford to ignore it. You can’t any longer. Remember - retirement doesn’t include promotions that come with big pay raises.

If I asked you what the prices of various goods were about three decades ago, you could probably rattle off some pretty accurate guesses. Let’s review what some of the prices were 30 years ago.

- Postage stamp: $0.25

- Gallon of gas: $0.97

- Average price of a new car: $15,350

I could go on, but you get the picture. What do those things cost today?

- Postage stamp: $0.55

- Gallon of gas: $2.73

- Average price of a new car: $36,590

Over the last 30 years, the price of most everything has at least doubled if not tripled. Historically speaking, we know that inflation is going to happen throughout our retirement, but we have a natural inclination to ignore it because it doesn’t happen overnight. We only really care about things that can and do happen overnight, not about what occurs over the long term despite the significant income erosion that inevitably occurs.

What follows below is a brief detour, but my purpose will become clear in a moment.

Two examples that I find psychologically fascinating:

First, we ignore inflation despite the fact that it’s been present in our lives the entire time we’ve been alive. We only care about what’s happening here and now. But if we look at the long-term, we can see the extremely powerful impact it could have on our long-term retirement.

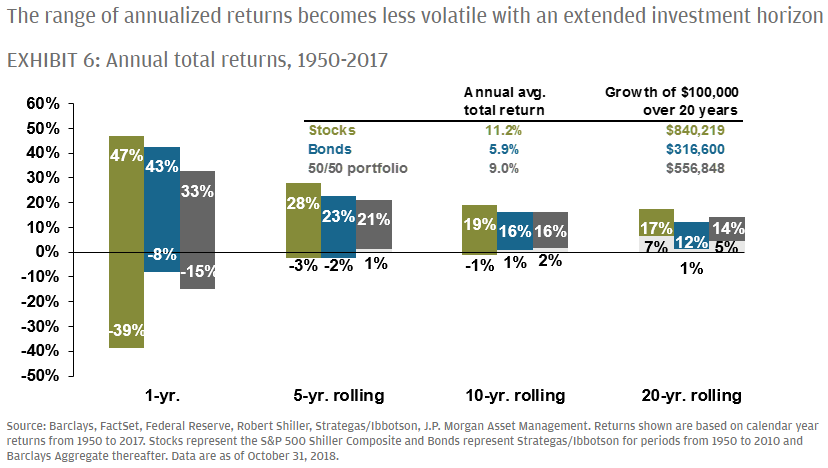

Secondly, we worry about the volatility of the stock market at any given moment because markets collapse quickly and investors often mistake it as a permanent loss of capital. Yet if we look at the long term, such as over the span of the career of today’s retirees, it’s clear that they’re worried about an issue that historically doesn’t even exist. Let’s look at what has historically occurred over various rolling periods in the following chart from JP Morgan.

As we can see, short-term volatility can be dramatic, but over the long term — which just about everyone reading this article should be concerned about — there hasn’t been little risk, there has been NO risk historically speaking.

This is not a way of saying this is what will occur over the coming twenty years, but it is a way of saying that this is the only thing that has occurred over nearly the entire time you’ve been alive.

For what it’s worth, I realize that two of the three biggest declines in the history of the stock market have occurred as you have been nearing the finish line (a blessing in disguise for dollar-cost averaging) so it’s still actively in your rearview mirror. But if you drive your car looking in your rearview mirror, eventually you will crash. Fighting the last battle is never a way to win a war.

Detour complete.

You must approach retirement planning with objectivity and a total understanding of the issues at hand that you will inevitably face as you move into your retirement years. Given the fact that inflation has been around for the entirety of our country’s history, it seems likely it will continue throughout your retirement as well.

But if you do nothing to prepare for this inevitability, you will likely seal your fate. You can choose to ignore these two issues or plead ignorance, but neither approach will help you. You must land on a portfolio approach that will provide the confidence you need to ensure, historically speaking, that you will have an ever increasing income stream that will grow as your income needs grow.

Then, and only then, can you possibly find comfort that longevity isn’t actually a risk, but a goal to strive for. A privilege where you might get to have a long relationship with your great-grandchildren.

Okay, you get it now. You know that you are likely to live a long life and that inflation can have a significant impact on that long life. What can you do about it? Let’s talk about a specific portfolio strategy that might ease some of the stresses that come with investing that can effectively address the impact inflation can have on a long life.

3) Properly investing your portfolio

Retirees crossing the finish line today are faced with a few issues that I believe are unique in their combination.

- Rising life expectancy and the accompanying inflation as we’ve already discussed.

- Historically low bond yields at the end of a 40-year bond bull market.

- Lastly, at current, we are still near a stock market peak.

Seem like an overwhelming set of circumstances? If I were picking a time to retire, this doesn’t seem like an ideal combination from which to start if you ask me.

Over the past few years, I’ve done a ton of research and reading about the issue of income creation for retirees. I’ve settled on four primary goals for every retiree portfolio (not necessarily in order of importance):

- A sustainable and growing income that keeps up with inflation.

- If possible, grow the underlying principal with less volatility.

- Allows you to focus on things that truly matter to you rather than what’s going on in the markets.

- Ultimately, peace of mind.

Is there a strategy that can theoretically accomplish all four effectively? I believe there is an evidence-based portfolio strategy that can effectively address the three circumstances above while accomplishing the four goals most retirees have in common. That is, dividend growth investing.

What Dividend Growth Investing Is Not

Before I get into the strategy itself, I think it would be smart to start with what dividend growth investing is not.

- It is not a thinly veiled attempt to “beat the market” (whatever that means anyway) — I wouldn’t rule the possibility out, I’m just saying it’s not the goal in any way whatsoever and want to be abundantly clear about that fact.

- It is not a foolproof way to eliminate behavioral investing mistakes — it surely should reduce the probability of those mistakes though.

- It is not designed to provide the highest yielding portfolio — while it may provide a yield higher than the overall market, it is not a “high yield” portfolio in a general sense.

- It is not an answer to every retiree’s prayers. Though I vehemently believe this is a viable way to build a portfolio for a thirty plus year retirement, the withdrawal expectation must still be reasonable with regard to the size of their portfolio amongst many other variables.

We are seeking a reliable income that has grown throughout history - in other words, an evidence-based income strategy. That said, no strategy is foolproof or guaranteed.

Goal #1: A sustainable and growing income that keeps up with inflation.

“You don’t take your account statement to the supermarket.” - Nick Murray

One benefit of dividend growth investing is it’s unique ability to maintain and even increase purchasing power over time. While most retirement income strategies rely on “price growth” (growth of the overall market) to provide the income needed, historically, dividends have done this without issue.

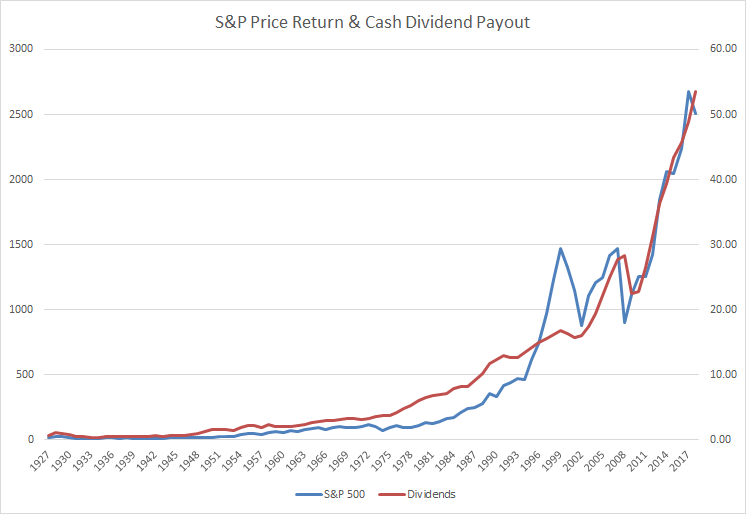

Remarkably, since 1960, while inflation averaged around 3% per year, the cash dividend paid by the S&P 500 index grew from $1.98 to $48.93 in 2017 for a compound annual growth rate of 5.79%. In other words, your dividend income would have almost doubled the rate of inflation through all sorts of market environments.

Below is a chart showing the price return of the S&P 500 since 1927 and the dividends paid over that same time. One thing worth noting is the remarkable stability of the cash dividend payment.

The only blip of note on the dividend payment line is during the Great Panic of 2008. Much of the 2008 dip though can be attributed to the banking sector - a story too convoluted to tell here. Amazingly though, during a period where the peak to trough drawdown of the market was about 57%, the dividend dip was just over 21%.

But remember, the chart above (and the 21% decline noted) is showing the dividend payment of the entire S&P 500, not the dividend growers - a significant distinction. In fact, there are 133 companies that have increased their dividend each year for 25 straight years. They are known as the Dividend Champions. For investors that were focused on dividend growth, it’s entirely possible that many investor’s dividend income kept growing despite the bloodbath.

One issue I think causes stress in the minds of retirees is the idea of “what to sell and when” to create the income they need depending on what’s going on in the market at the time. One of the primary benefits of the dividend growth strategy is that the goal is to leave the principal totally intact. In other words, we’ll continue to own the companies, we’ll just collect the paycheck each and every quarter. This effectively removes the worry of “what to sell and when.”

Retirees tend to make the biggest portfolio mistakes when focusing on stock prices because a falling stock market engenders fear. If your income relies on price - because you have to sell something to generate the income you need - then you’ll likely always be fearful of any and all downward market volatility. Alternatively, if you are approaching your portfolio as an owner/partner in a business seeking a reliable income stream, you are less likely to make emotional buy and sell decisions.

Goal #2: If Possible, Grow the Underlying Principal with Less Volatility

Regardless of strategy, retirees are going to worry about their account balance. It’s just something I’ve come to terms with. While dividend growth investing can provide a buoy in the storm via a steady income stream, retirees are often seeking a combination of lower volatility and price growth. And in many cases, they are willing to give up some upside for some downside protection.

The beauty of dividend growth investing is that it can provide both as well. Because you are still investing in the ownership of companies, these companies tend to grow over time - albeit at a slower rate than many companies that are new to the scene. Because these companies are more mature in nature, they tend to have more stable cash flow from which to pay dividends and are therefore historically less volatile.

I’d like to draw your attention to the columns Beta and Standard Deviation. These are two measures of volatility - the lower they are, the less volatility one should hypothetically have. As you can see, dividend growers and initiators have the lowest measures of volatility amongst the mix here.

I want to make a quick note about the “Returns” column as I do not believe it tells the whole story. I view dividend growth investing as a viable retirement strategy because of the income that it can provide, not because it is the best performing asset class.

And to say that dividend growers are the best performing asset class would actually be incorrect anyway - it is the best of those noted above, but it ignores the “asset class” of total shareholder yield (dividends plus share buybacks). It’s been shown before that total shareholder yield is actually the best performing group. I don’t need to get into that here, I just want to be overtly upfront about this oversight based on the data above and to prove that if you torture the data enough, you can make it say anything you want.

To be clear, the goal here is not total return, but income. There is an argument for total return, but going back to my belief of not wanting to make the decision of what to sell and when, I tend to believe that dividend growth investing has the best behavioral outcomes and therefore provides more peace of mind for the retiring investor.

Goal #3: Allows you to focus on things that truly matter to you rather than what’s going on in the markets.

If your income needs are properly addressed via a historically reliable dividend income stream that is roughly keeping pace with inflation, if not outpacing inflation, there is little need to worry about the underlying principal.

By nature of investing in these types of mature companies, your portfolio is likely to be a who’s who of stable companies. I still believe in the indexing nature of this strategy to eliminate any individual company risks that might exist because we’ve all seen the mighty fall more than a few times.

And yes, to be sure, the principal value will fluctuate, but if you’re focused on the income, you may not even notice if you manage to avoid the news.

If your income is reliable, you are less likely to make emotional changes to your portfolio when everyone around you is in total meltdown mode. You can keep planning your trips and hanging out with the grandkids which I think is a much more sensible way to go about planning.

Goal #4: Peace of Mind

Nobody, including myself, can ensure peace of mind when it comes to retirement planning. But for all the reasons noted above, assuming reasonable withdrawal assumptions, I tend to believe that dividend growth investing when paired with a sensible rainy day fund can provide virtually all of the income needed with little regard to principal value at any given moment.

And for retirees, what more could you ask for?

Downsides of Dividend Growth Investing

I think in order to offer a fair and balanced perspective, it’s important to note the potential shortfalls of any strategy, perhaps even more so when I’m advocating for said strategy. Here are the areas I’ve noted that could be viewed as potential issues:

- Generally, your portfolio is likely to end up being quite concentrated in U.S. Large Cap companies.

- In taxable accounts, if you are receiving non-qualified dividends, they are taxed at ordinary income tax rates. (This is generally from non-U.S. companies and those that have not been owned long enough to qualify.)

- In taxable accounts, all dividends received (qualified and nonqualified regardless of whether paid out or reinvested) are taxed in the year received.

- Potentially, you could end up with a higher allocation to stocks, but this depends entirely on your personal financial situation and preferences.

- Because most companies that pay increasing dividends are mature companies, you may miss out on the “big winners” that everyone seems to be searching for.

None of those issues do I personally have an issue with, but I wanted to be sure they were stated outright.

Closing

To close my longest post ever, a quick recap - you will probably live a long time and as a result, you will face inflation that will require your income to grow with it if you want to maintain your standard of living. This requires an approach to portfolio planning that can address those issues concurrently and I believe dividend growth investing to be a worthy candidate for your retirement planning needs and consideration.

Long story short, there is real beauty in simplicity, especially when it comes to creating a sustainable paycheck in retirement. While I can’t recommend any specific funds or stocks that can help you achieve this simple, yet overly effective retirement income strategy, I will recommend a book worth reading if you’re at all interested in the nitty-gritty of dividend growth investing.

That is, The Case for Dividend Growth by David L Bahnsen.

Thanks for staying with me to the end!

Ashby Daniels

Best of luck in your retirement planning. If I can answer any questions for you, feel free to Contact Me. Or if you think you might be a fit for our practice, see Who We Serve.

[1] Data from NYU Stern School of Business

Disclaimer: Opinions expressed are those of the author and are not necessarily those of Raymond James. All opinions are as of this date and are subject to change without notice. Dividends are not guaranteed and must be authorized by the company’s board of directors. Any information provided is for informational purposes only and does not constitute a recommendation. Future investment performance cannot be guaranteed, investment yields will fluctuate with market conditions. Keep in mind that there is no assurance that any strategy will ultimately be successful or profitable nor protect against a loss.