Many pundits and market experts (if there is such a thing) have been forecasting below average market returns for a couple of years now. Interestingly, since this started becoming a “thing” around 2018, the market returned 31% in 2019 and 18% in 2020. It’s not important to the topic of this post, I just think it’s funny.

The idea that future returns will be lower is widely accepted. I’m not saying I disagree with the premise as P/Es are a bit stretched at the moment. Equities aren’t necessarily overpriced in relation to bonds, but that doesn’t mean equities are cheap. They’re just cheaper than bonds at the moment. But nominal market returns aren’t what matter anyway.

It’s the relationship between inflation and nominal market return that matters, not the nominal return itself. Let’s look at two time periods as a comparative example.

1968-1988:

Nominal Market Return with Dividend Reinvestment: 9.58%

Inflation Rate: 6.22%

Real Return: 3.36%

1999-2019

Nominal Market Return with Dividend Reinvestment: 6.53%

Inflation Rate: 2.16%

Real Return: 4.37%

These are, more or less, cherry-picked time periods of 20 years each to illustrate a point. Even in a period where the nominal return was over 3% less, the real return was actually a full percentage point higher in the second period than the first.

So, is it possible that forward-looking returns might look something like 1999-2019? Of course, it’s possible. Does that mean the real return will be paltry as a result? Possibly not if inflation remains low.

One additional point about real returns and why they are SO important…

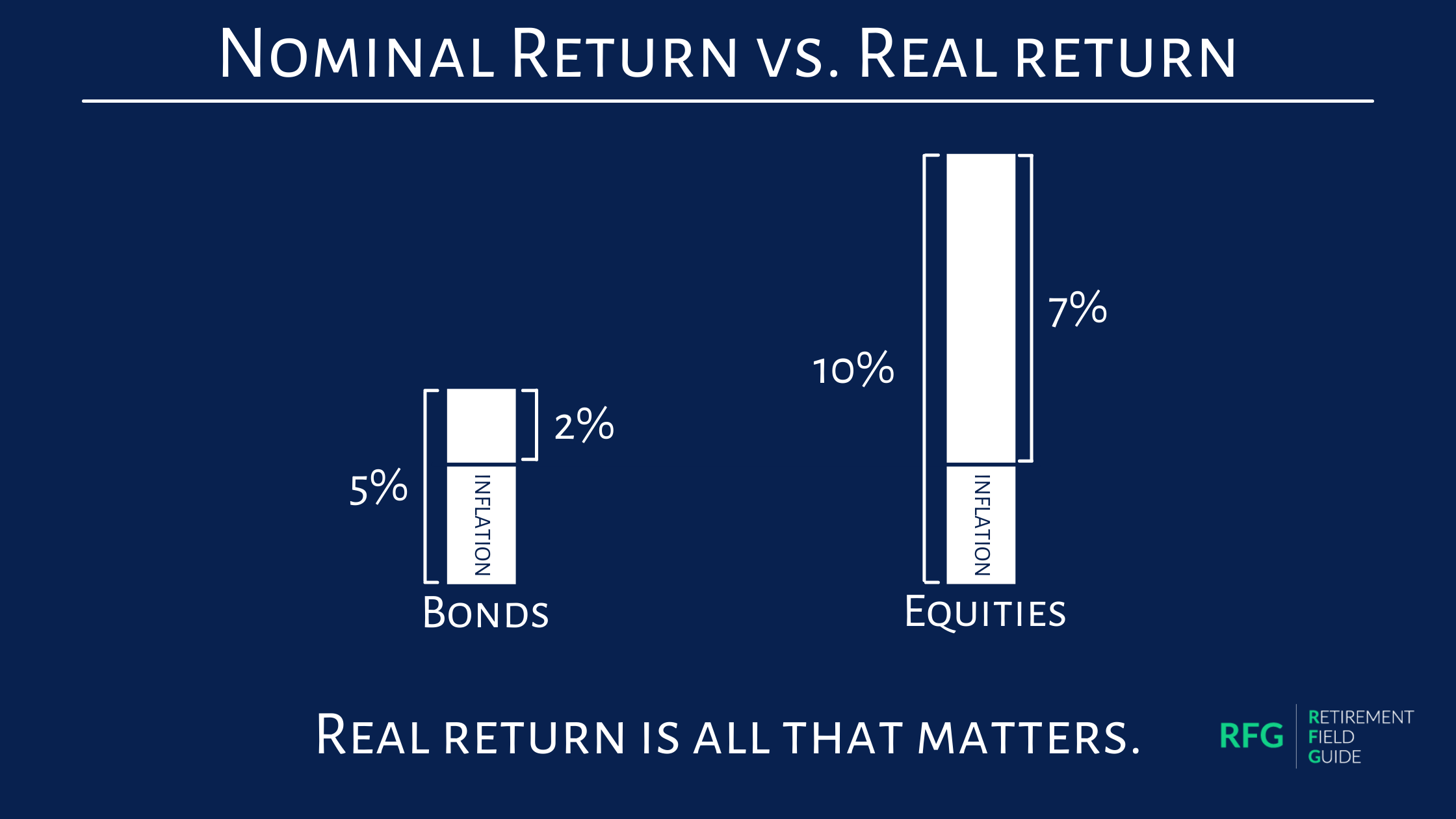

As Ben Carlson noted in his post “Stock, Bond & Cash Returns: 1928-2020,” the annual returns of equities since 1928 has been almost 10%, while the return of bonds has been almost 5%. Inflation during the same period has been about 3%.

If equities have returned 10% and bonds have returned 5%, on the surface, it appears that equities have returned twice as much. That’s true on a nominal basis, but real return is what buys the groceries.

So, if inflation has been about 3%, then the real return for each asset class has been 7% for equities vs. just 2% for bonds. That means that equities haven’t outpaced bonds by 2X, but by 3.5X!

What does this mean for where we are at today? It’s possible that forward-looking equity returns may be lower, but if inflation remains low, it may be inconsequential. As for bonds, given where interest rates are today, I can’t imagine a worse starting point for bonds than exists right now on a forward-looking basis regardless of what happens with inflation. Will bonds return anything close to their historical average of 5% nominal or 2% real? It seems unlikely to me.

And in the long run, real return is all that matters.

Stay the course,

Ashby

If you liked this post, consider subscribing down below. 👇👇

This post is not advice. Please see additional disclaimers.